Polyester markets ended June recovering previous losses

Polyester markets in Asia ended the last week of June mostly recovering, partially or fully, the losses of third week after the trade war between US and China created a kind of upheaval in upstream markets. However, stronger US$ pegged local values down equivalent in US$ term.

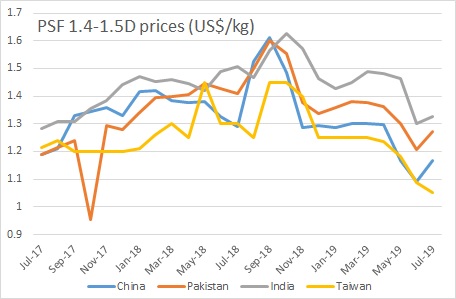

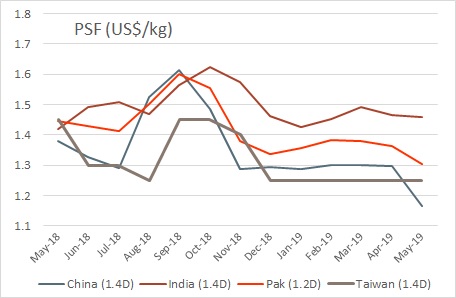

Polyester staple fibre (PSF) prices were seen rising in China but weak Yuan pegged flat to down in US$ terms. The markets were supported by rising crude oil and raw material prices up. In Pakistan, PSF market sentiment remained flat and producers’ offers rolled over. Indian PSF prices were reduced as buyers postponed buying due to weak demand. Downstream, polyester yarn markets were stable in China, Pakistan and India seeing input cost rebounding along with crude oil values.

PET chip prices firmed up in China as sales-production status improved with chip-based spinning mills making some replenishment. As crude oil surged and semi dull chip makers pushing up offers, trading sentiment picked up with large parcels changing hands. European PET market was in disarray and demand appeared disappointing while availability worsened with BP failing to resume PTA production. This may impact 2019 contract negotiations.

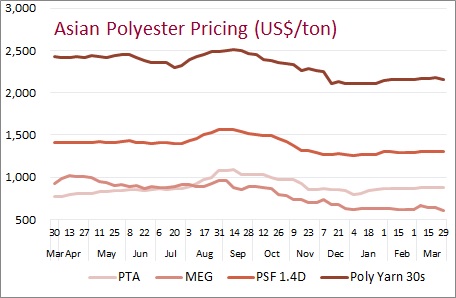

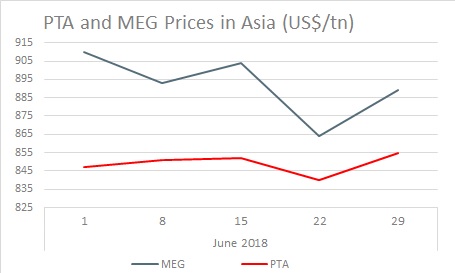

PTA prices surged somewhat in Asia recovering earlier losses completely this week. In China, PTA futures picked up directly and the values jumped, driven by a sharp rise for crude oil values. In Europe, PTA supply was still marred by production problems, despite issues being slowly resolved. Feedstock, paraxylene prices in Asia regained previous week’s fall as the market enter Q3 when downstream operating rates are high amid good margins. Meanwhile no settlement was reached for July as well as June contracts. In Europe, spot paraxylene gained on Asian cues while domestic demand remained weak. In US, spot edged lower falling slightly on the lower end of the range, amid limited activity.

Also read PTA makers enjoying healthy margins, but will they continue?

MEG market continued to fluctuate upward in Asia driven by favorable PTA market and rumors about some MEG plant issue. Inventories along China eastern coast also declined 4% week on week to 779 kilo ton. In Europe, MEG market was divided as players continued to await June contract price confirmation on the final day of the month. In US, MEG domestic consumption was slow because of co-feedstock issues were affecting downstream PET production. The market is likely to face downward pressure in July as plant maintenance season wraps up.

Meanwhile Asian ethylene markets continued their flat run for the third week in a row with prices rolling over across region. Buyers remained on the sidelines amid sluggish crude oil futures while sellers were reluctant to reduce offers as thy saw limited spot availability. In Europe, spot ethylene prices surged midweek although July contract price settled down from June. In US, ethylene prices were relatively steady in narrow range as the market awaited the start-up of two new crackers, which will further expand supply.

For detail report write to us at sales@textilebeacon.com or visit us at textilebeacon.com for sample report