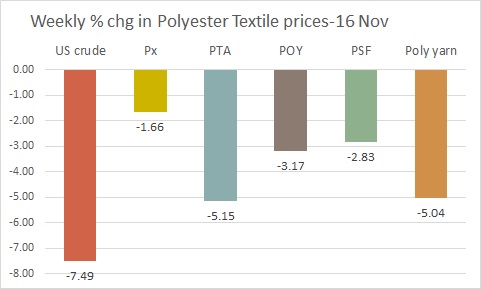

Polyester textile prices decelerate in second week of November

Polyester textile prices have been on the down trend in recent week and were seen decelerating in the second full week of November that ended 16 November. Again both upstream and downstream segment looked at each other for support. However, the extreme upper end of polyester textile, the crude oil markets, were subdued and the effect percolated into its derivatives. At the extreme lower end, the fabric market sentiment was flat, with unchanged operating rates. So, demand was hard to improve despite falling prices. This can be attributed to end of peak season, a normal phenomena year after year in polyester textile markets. The garment industry is in its logistical activity to deliver goods to retailers before the break of Christmas and New year festival.

In the week ended 16 November, polyester staple fibre (PSF) markets in Asia succumbed to persistent fall in raw material costs but were seen steadying on weekend as feedstock markets rebounded slightly. In China, polyester prices declined in first half but sentiment appeared mixed later as major producers’ hiked offers. In Pakistan, producers reduced offers by more than 5% week on week for the second straight week while Indian prices were cut 6% for second half November.

Polyester spun yarn markets in Asia were pounded by falling PSF cost on back of easing feedstock. The markets were off the peak season, and typically moderates during this phase. In China, margins were squeezed as yarn prices declined more rapidly than PSF prices. In Pakistan, yarn producers were seen passing on some of the reduction in PSF by cutting yarn prices. Similarly, Indian yarn prices also declined reflecting reduced prices of PSF for November.

Polyester filament yarn (PFY) markets in China extended the declines as prices fell sharply initially in the week but remained steady later. With PTA futures boosting local sentiment at weekend, downstream mills increased buying to some extent. In Pakistan, offers for imported goods fell and local offers were revised to parity. Sentiment warmed up a bit as a result. In India, POY market sentiment was stalemated and offers were cut 4% week on week to boost demand, with deals negotiable based on volumes.

Polyester fibre chip markets in Asia were in wait-and-see sentiment as offers and discussions declined sharply on the back of soft feedstock but with positive cash margins, producers were active to offload goods. The slump in Asian markets and expectations of lower production costs resulted in more flexibility to Europe PET market. Meanwhile demand for PET in Europe remained subdued.

Purified terephthalic acid (PTA) markets continued to remain in correction in Asia and prices easily fell as difficulty to rise was much strong amid bearish trend in paraxylene markets. In Europe, November contract decreased as the settlement moved alongside upstream paraxylene November contract

Asian paraxylene markets were dragged lower by firm selling interest for both December and January delivery cargoes, while weakness in the downstream PTA market weighed on the market. In Europe, November contract settled down on back of falling Asian prices and despite a fairly tight market. In US, spot fell to its lowest levels since early August, tracking declining prices in Asia, improved supply and muted demand amid seasonal downturn.

(Source: Global Markets Weekly Review. For full report write to us at sales@textilebeacon.com)