Nylon prices rising but are still below year ago level

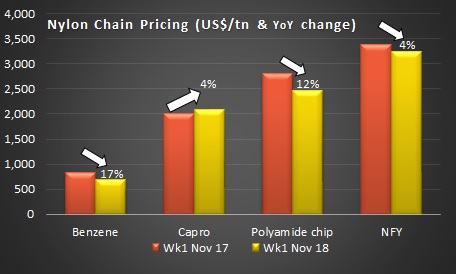

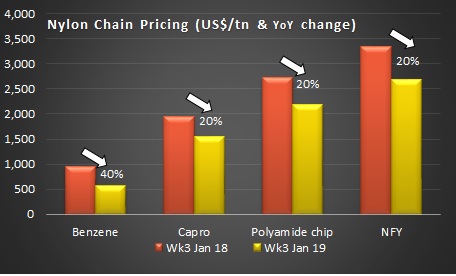

Nylon prices rose in the week ending 18 January 2018, but were still below their year ago level. Almost the entire nylon price chain were on similar trend. Benzene prices were down 40% year on year across regions, making Europe the cheapest benzene markets and US the highest. Caprolactum, a derivative of benzene, was cheaper by 20% in Asian leading to nylon chip and filament yarn values to follow through.

Nylon filament yarn prices were seen rising in the third week of January for few specs in China amid surging chip values and rising caprolactum (CPL) cost. Noticeably, FDY prices moved up while DTY prices held stable. Meanwhile, supply tightened before the Spring Festival, and prices generally held ground.

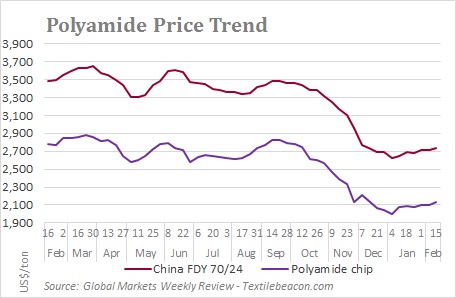

Nylon or polyamide chip prices surged in China while they were steady in other Asian markets. The surge can be explained by the rising CPL cost and improvement in downstream buying activity ahead of Lunar New Year holidays. Suppliers stuck to their offers, amid cautious buying interest at high-end.

CPL market held stable run on moderate demand and steady benzene prices. In China, prices for domestic liquid goods rebounded while those for flake goods rolled over. In contract, both Sinopec and Fibrant raised their January contract nominations for liquid goods by 1.5%.

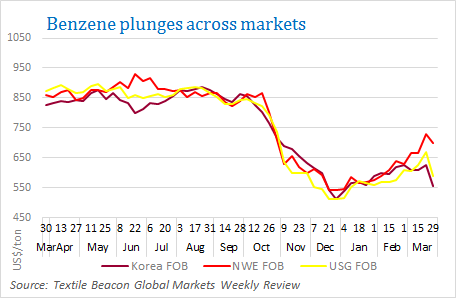

Asian benzene prices moved within a narrow range lacking definitive direction. Market activity started to taper off ahead of the Lunar New Year holiday. Meanwhile, inventories along eastern China increased to 200.5 kilo ton. In Europe, benzene market was thinly traded, with February prices in contango and expectations of reduced length and healthier demand in the forward months. In US, spot prices rose for second consecutive week as market showed some signs of rebalancing.

Forecast for January

Nylon demand in Asia is expected to remain weak during the current winter months as the warm weather dampened replenishing for winter apparel. Thus, nylon prices are likely to stay soft in January and through Q1, as demand is expected to stay weak while supply will increase further owing to plant expansions in China. The market is not expected to improve in the near term, given the ensuing US-China trade row. Meanwhile, domestic prices for caprolactum and conventional grade nylon chips were at almost parity in China. Producers will strive to maintain healthy margin levels between caprolactum and nylon prices, adjusting their input variables.

Source: Global Markets Weekly Review, Global Nylon Price Forecast – Monthly Report