Cotton will take time to rise now until demand makes up

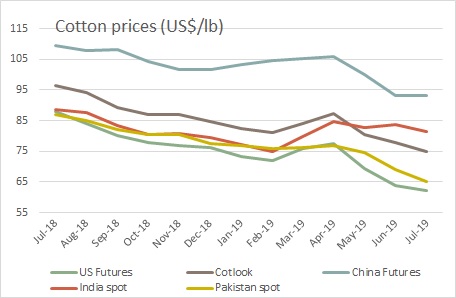

Cotton price momentum is demolished by two key factors in recent time – expected larger harvest and the US-China trade war. Both have been languishing the cotton market with latter for almost more than a year now and the former which is raising its head now. The US Cotton futures on the ICE have fallen to a 3-year low while the spot benchmark, the Cotlook ‘A’ index is at a multi-year low.

The USDA in its latest August report has highlighted higher opening stocks, production, exports and ending stocks for US. Production for 2019 crop is raised 2% to 22.5 million bales on NASS’s first survey-based production forecast. The survey indicates slightly higher area and yield compared with last month’s expectations, resulting in the largest crop in 14 years.

Opening stocks are raised 250,000 bales due to lower-than-expected 2018-19 exports. Exports for 2019-20 are also raised 200,000 bales this month, and ending stocks are raised 500,000 bales to 7.2 million. The 2019-20 season-average price for upland cotton is forecast at US cents 60 per pound, down US cents 3 from last month.

It has also projected lower world cotton consumption largely on account of a 2.0-million-bale increase in 2019-20 global ending stocks from the July forecast. World opening stocks are higher, largely due to a 500,000-bale decline in 2018-19 consumption. Production in 2019-20 is forecast 200,000 bales lower this month, but higher beginning stocks and a 1.2-million-bale decline in projected consumption were more than offsetting. Consumption is lower in China, India and Uzbekistan.

At the moment, demand remains a big cause of concern for cotton market. World demand has been less this year as China has stopped buying, resulting in lower world prices. In China, cotton prices hit 10-year low, pressured by weak US Futures for the white fibre and escalating US-China trade tensions. Reports have cited high cotton stocks in China and plunging US prices for the current decline, as well as signs the trade war between the two unlikely to end any time soon. China is a major exporter of cotton-based textiles to the US and there are fears of extra duties on Chinese textile products in fresh tariffs on around US$300 billion of goods.

To aggravate the situation, Indian spinners have started cutting back on operations. Textile mills have slashed output by around 20% by cutting down operations by seven days a month after failing to absorb rising cost of raw materials and dampening yarn demand. Many mills have even reduced working shifts to one a day as against full operations earlier after the surge in operating cost squeezing margins and escalated liabilities amid financial constraints.

Global demand for textiles will remain subdued in months to come. Demand will be adversely affected by a reduction in purchasing power as a fall out of slowing global economy and a paradoxical trade situation. While US has been stubborn on its demand from China, the Chinese government has been responding equally.

The events clearly suggest that there will be decline in textile production which is already eminent now, and an imminent demand squeeze. For demand to recover, the global economic situation and the impediment arising from the US-China trade war needs to improve at a much faster pace. Meanwhile, cotton markets will be at the mercy of the two factors mentioned earlier.

Source: Global Markets Weekly Review