Cotton and cotton yarn market behavior in second week of November

Cotton markets were full of activities as arrivals have started flooding in mandis in India, an usual characteristic of this period. Prices have started receding from their peak in most domestic and international markets barring a few.

Globally two eventualities in cotton markets may work in support of prices. One, if Indian government procures cotton in line with MSP, which will reduce export surplus and support international prices as seen in the past. Two, in case China imports more than 1 million ton of WTO mandated quota, this would also lend support to markets. But, as of now there is no indication of such event happening as China is heading for the large harvest, in excess of 5 million ton, and it still holds significant stock in government reserve.

In the week of 10 November

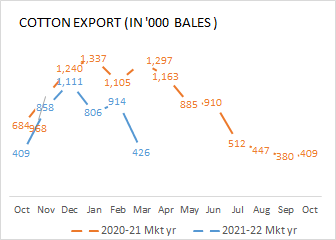

Let us decipher what happened in the week ended 10 November in Indian cotton markets, which also coincides with the completion of one year of demonetisation. Cotton arrivals have started picking up rapidly (touching about 1.30 lakh bales daily this week) in all major centres. The Cotton Corporation of India (CCI) has started buying in places where spot prices have equaled the Minimum Support Price (MSP). According to reports, CCI plans to buy 100 lakh bales this year at both MSP prices and through commercial purchase. The minimum support price pegged for Shankar 6 is INR4,270 a quintal and for Bunny/Brahma, INR4,320 a quintal.

In the second week of November, a period of increasing arrivals, cotton prices continued to move in different directions with coarser spec (Deshi and V-797 types) cotton surging INR 100-300 per candy while finer cotton cheaper by INR 200-900 per candy. Benchmark, Shanker-6 was traded at INR37,200 per candy, down INR900 from week ago.

In the second week of November, a period of increasing arrivals, cotton prices continued to move in different directions with coarser spec (Deshi and V-797 types) cotton surging INR 100-300 per candy while finer cotton cheaper by INR 200-900 per candy. Benchmark, Shanker-6 was traded at INR37,200 per candy, down INR900 from week ago.

With India’s cotton harvest estimated at over 385 lakh bales this year, prices are expected to come under stress especially for Shankar 6, BB varieties. With arrivals rising, prices have already fallen and are expected will drop further when the arrivals peak to 2-2.5 lakh bales a day by the end of this month.

In global market, US cotton futures on the ICE posted the biggest one-day percentage gain on 10 November, supported by buying amid December options expiry and mill fixations, and was up on the fortnight. Contracts for March settled at US cents 69.14 per pound, up 1.59% or US cents 1.03 from end-October. The USDA, in its latest monthly crop supply and demand report, raised US production estimates to 21.38 million bales from 21.12 million bales in the previous month, highlighting the resilience of this year’s crop against threatening weather, numerous hurricanes and freeze events. The report also said that the ending stocks in US will be the largest since 2009-10, a 122% increase year-over-year at 6.1 million bales. An earlier report had stated that 46% of cotton crop was harvested in the US by end October.

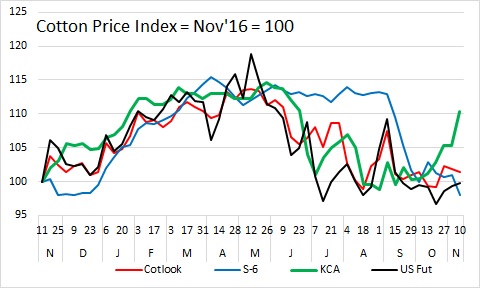

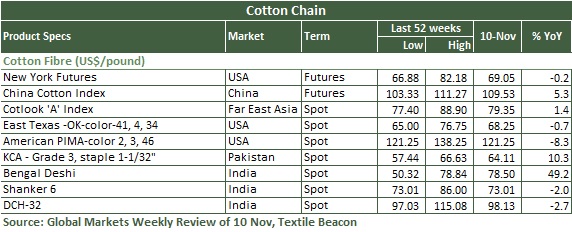

The China Cotton Index retreated slightly in the second week of November to 16,001 Yuan a ton or US cents 110 per pound. A government announcement stated that it will not, in principle, purchase cotton for state reserve during the new cotton arrival period (till the end of February 2018), leading to bearish sentiment in cotton market. On state reserve policy, sales will start from 12 March and will continue until end of August with the daily auction volumes no more than 30,000 tons. If prices of domestic and international cotton rise markedly and rapidly for a period of time and the turnover rate of the reserved cotton auction exceeds 70% for more than three days a week, measures like increasing daily auction volume and extending the sales period will be taken to ensure market supply.

As of 9 November, a total of 23 lakh tons of lint was pressed nationwide in China, consisting of 8 lakh tons from XPCC, 15 lakh tons from Xinjiang local cooperative system and 0.33 lakh tons from inland.

In Pakistan, trading activity dropped gradually during the week ended 10 November on the Karachi Cotton Exchange, while spot rate remained unchanged and firm at PakRs6,745 per maund ex-Karachi. Meanwhile reports indicate that Import deals of 1.6 million bales were concluded due to shortage against the total of 2.5 million bales accepted. The Central Cotton Assessment Committee in its last meeting lowered cotton production estimate from 14.1 million bales to 12.6 million bales. However, given the condition of the standing crop, trade estimates peg output at only 12 million bales. Meanwhile, the All Pakistan Textile Mills Association has urged the government to allow imports of Indian cotton on reduced duty rate.

Spot benchmark, Cotlook A index however, lost US cent 0.75 in the first half November from H2 October at US cents 79.35 per pound.

Cotton yarn

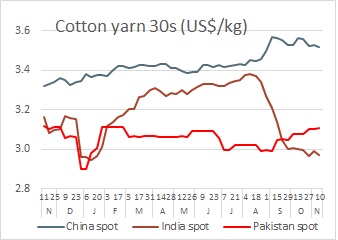

Cotton yarn trading sentiment extended previous trend and prices were divergent in China. However, the markets showed sign of weakness with demand for open-ended yarn slackened but tolerable and conventional cotton yarn was relatively weak. Demand for weaving yarn was better than that for knitting. Prices were mostly stable with some specs declining. In India, cotton yarn prices remained stuck, irrespective of fresh decline in cotton price of late. Stability is attributed to low margins for spinning mills. Export prices have slightly increased US cents 2 a kg during the week, given the currency weakness. In Pakistan, cotton and yarn prices moved in different directions. While cotton prices strongly rose, yarn prices remained unchanged on the Faisalabad yarn market, seeing strong demand. However, export prices were slightly down due to weak export demand.

Cotton yarn trading sentiment extended previous trend and prices were divergent in China. However, the markets showed sign of weakness with demand for open-ended yarn slackened but tolerable and conventional cotton yarn was relatively weak. Demand for weaving yarn was better than that for knitting. Prices were mostly stable with some specs declining. In India, cotton yarn prices remained stuck, irrespective of fresh decline in cotton price of late. Stability is attributed to low margins for spinning mills. Export prices have slightly increased US cents 2 a kg during the week, given the currency weakness. In Pakistan, cotton and yarn prices moved in different directions. While cotton prices strongly rose, yarn prices remained unchanged on the Faisalabad yarn market, seeing strong demand. However, export prices were slightly down due to weak export demand.

SOURCE: Global Markets Weekly Review of 10 November 2017